Q3 2025 | Market Update

The S&P 500 and S&P/TSX Composite rose over the quarter, yet investors favoured safe haven stocks less likely to be impacted by economic turbulence.

Highlights

- With worst-case tariff scenarios potentially avoided, equity markets continued to reach new all-time highs.

- The economy cooled just enough to bring additional central bank stimulus but not enough to be concerned about a recession.

- Active management remains key as weakening economic data should eventually broaden market participation across sectors and geographies.

Equity markets rise as tariff concerns ease

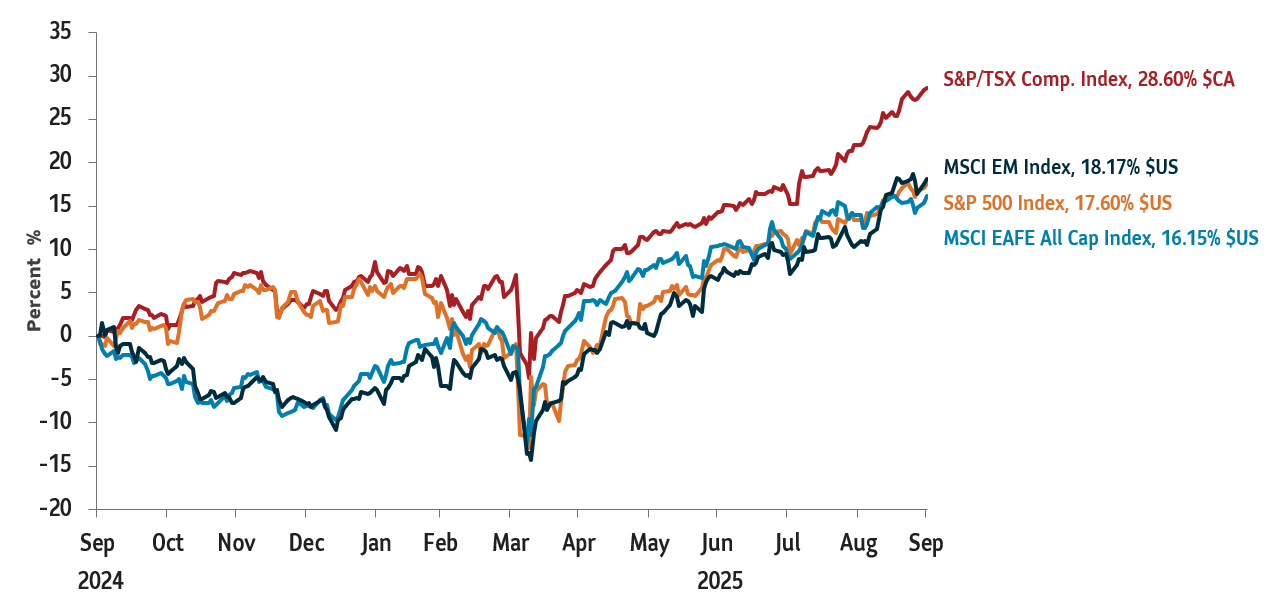

Equity markets had a strong quarter as worst-case fears around tariffs began to recede, with many indexes posting double-digit returns in Canadian-dollar terms. After an initial markdown, earnings expectations for many major indexes recovered to the levels expected prior to Liberation Day.

Cooling economic data led to the U.S. Federal Reserve (Fed) resuming rate cuts in September after a nine-month pause, fuelling debate about the impact on rate-sensitive stocks and the potential for some sector rotation. The Bank of Canada also lowered rates in September, with more cuts expected as Canadian economic data deteriorated due to the impact of tariffs. Canadian inflation remained subdued compared to the U.S., while unemployment rose, with an especially notable increase in jobless youth.

The S&P 500 Index rose 8.1%1 (USD) on a total return basis over the quarter. Canadian equities also rose, with the S&P/TSX Composite Index gaining 12.5%1 on a total return basis in Q3 to reach a new all-time high. Despite record-high equities, investor behaviour remained defensive, with market performance driven by safe haven mega-cap technology and AI stocks, which are more likely to weather a recession. This divergence between investor behaviour and market prices raises questions about the sustainability of AI/tech sector outperformance.

Value stocks lagged, with speculation that further central bank rate cuts could spark a rotation into this area. Mergers and acquisitions activity picked up over the quarter as interest rates fell. Tensions escalated in Israel-Gaza and in Russia-Ukraine, but this had little impact on financial markets.

Graph 1: Equity markets continue to reach new all-time highs

Total return, indexed to 0 as of September 30, 2024

Source: Bloomberg data as of September 30, 2025.

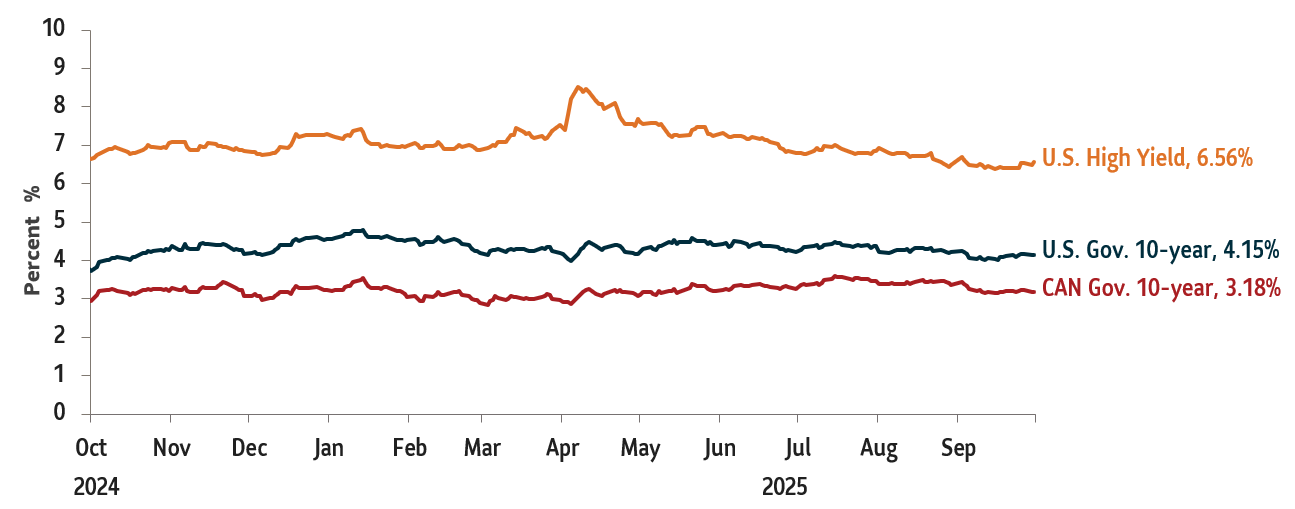

Fixed income markets also gained over the quarter, with yields generally falling. The benchmark 10-year U.S. Treasury yield ended the quarter with a yield of 4.15%, up 31 basis points (bps) from last quarter.1

Credit markets remained stable, but credit analysts flagged cracks emerging in private credit and a rising risk of the market overheating. Global corporate defaults and U.S. consumer delinquency rates were closely watched as indicators of credit health. The potential for higher mortgage defaults in Canada will be something to watch next quarter.

Chart 2: Bond yields fall as labour markets cool

U.S. and Canada 10-year bond yields

Source: Bloomberg data as of September 30, 2025.

The Canadian and U.S. economies are cooling just enough to potentially bring additional interest rate cuts, but not enough to raise recession concerns. We’re watching leading labour market indicators in both countries, which could be pointing to something a bit worse to come. Also top of mind for where markets may go next are Fed rate decisions, inflation data, consumer spending trends, credit market defaults, and any shifts in investor sentiment or sector leadership.

The tariff picture is still unclear. A challenge of the use of International Emergency Economic Powers Act comes before the U.S. Supreme Court on November 5, while multiple sector-specific tariffs are under review and new sector-specific tariffs continue to be announced.

Gold has shown great resilience against some of the volatility this year. It has also benefited from the longer-term theme of investors broadening their exposure to different currencies and different markets. Gold now fits into the category of an additional reserve currency for central banks and a safe haven for investors. We continue to hold gold as a tactical position in the portfolios.

Key tactical changes

- Remained tactically overweight in gold: Gold reached a new all-time high amid declining real yields, currency market fluctuations and ongoing geopolitical uncertainty.

- Adjusted U.S. sector rotation strategy: We allocated into specific sectors for a defensive positioning.

1 Source: Bloomberg data as of September 30, 2025.

Views expressed regarding a particular company, security, industry or market sector should not be considered an indication of trading intent of any mutual funds managed by SLGI Asset Management Inc. These views are subject to change and are not to be considered as investment advice nor should they be considered a recommendation to buy or sell. This commentary is provided for information purposes only and is not intended to provide specific individual financial, investment, tax or legal advice. Information contained in this commentary has been compiled from sources believed to be reliable, but no representation or warranty, express or implied, is made with respect to its timeliness or accuracy.

This commentary may contain forward-looking statements about the economy and markets, their future performance, strategies or prospects or events and are subject to uncertainties that could cause actual results to differ materially from those expressed or implied in such statements. Forward-looking statements are not guarantees of future performance and are speculative in nature and cannot be relied upon.