Is your cash for short or long-term?

Does market volatility worry you? Or does letting your money sit in cash seem the best choice given today’s economy? You may even have put some of your dollars in a money market fund, high interest savings accounts or a Guaranteed Investment Certificate (GIC), as many Canadians find these types of investments attractive.

Over the past few years, cash, high interest savings accounts and GIC yields may have been attractive because of higher interest rates. Many investors think of these types of investments as more secure. But it’s important to consider that this choice may impact your longer-term goals. Here’s why.

Historically, other asset classes have outperformed over the long run, including stocks and bonds, but they may carry more short-term risk. However, over the long term, their benefits are clear.

Canadian 91-day T-bill:

- 15-year total return: Approximately 48% as of May 31, 2025, with a 2.64% annualized return.

- 20-year total return: Roughly 68% as of May 31, 2025, with an annualized return of around 2.64%.

FTSE Canadian Bond Index:

- 15-year total return: Roughly 57% as of May 31, 2025, or about a 3.05% annualized return.

- 20-year total return: Approximately 98% as of May 31, 2025, with an annualized return of about 3.5%.

S&P/TSX Composite Index:

- 15-year total return: Approximately 248% as of May 31, 2025 which translates to about an 8.68% annualized return.

- 20-year total return: Roughly 391% as of May 31, 2025, which gives an annualized return of around an 8.25%.

S&P 500 :

- 15-year total return: Approximately 759% as of May 31, 2025, translating to about 16.15% annualized.

- 20-year total return: Roughly 704% as of May 31, 2025, which translates to an annualized return of around 10.97%.

For illustrative purposes only. Returns have been rounded to the nearest whole number for simplicity. Past performance is no guarantee of future results. It is not possible to invest in an index. Actual returns would be different due to fees and expenses associated with investing which are not applicable to an index.

Source: SLGI calculations from Morningstar Direct data, as of May 31, 2025. Returns in Canadian dollars. Returns have been rounded to the nearest whole number for simplicity

Considerations - Cash & GICs vs. longer-term investments

- Recently higher yields may have attracted some of your dollars.

- Cash and GICs may be perceived to be a risk-free place to park savings. However, they may not provide the long-term performance results that your portfolio needs.

- Other asset classes have the potential provide greater opportunities to earn greater gains over the long-term.

- Have your recent contributions been swayed by attractive yields?

- Are you off track from your longer-term savings goals and investment objectives?

Are you missing out? You may already have!

If you have money sitting in cash, a money market fund, high interest savings accounts or variable rate GICs, with recent rate cuts, interest rates in these may have followed suit. Following five rate cuts in 2024, the Bank of Canada kicked off 2025 with another rate cut in January. Tariffs threats from the U.S. has put some shadows on the Canadian economy since then. The Bank of Canada has paused cutting rates, although more cuts may be on the way to support the economy.

In a rate-cutting environment, bonds with longer maturity dates benefit significantly from a price increase or capital gain. Interest rates and bond prices move in opposite directions. So when rates go down, bond prices go up, plus you may get recurring interest payments. Now may be the time to move to longer-term assets since short-term cash-like instruments rates are decreasing in tandem with the Bank of Canada’s interest rate reductions.

If we look at the FTSE Canada 91-day treasury bill as a proxy, rates fell from 5.05% at the December, 2023 to 2.64% as of end of April 2025- that is reduction of 2.41% in just 14 months. (Source: Bank of Canada, Treasury bill auction – average yields – 3 month: https://www.bankofcanada.ca/rates/interest-rates/t-bill-yields/)

The Bank of Canada may cut rates even more – especially if the economy struggles. If you don’t need your principal protected and can afford to take some risk, consider what you might be missing out on by investing in cash-like instruments.

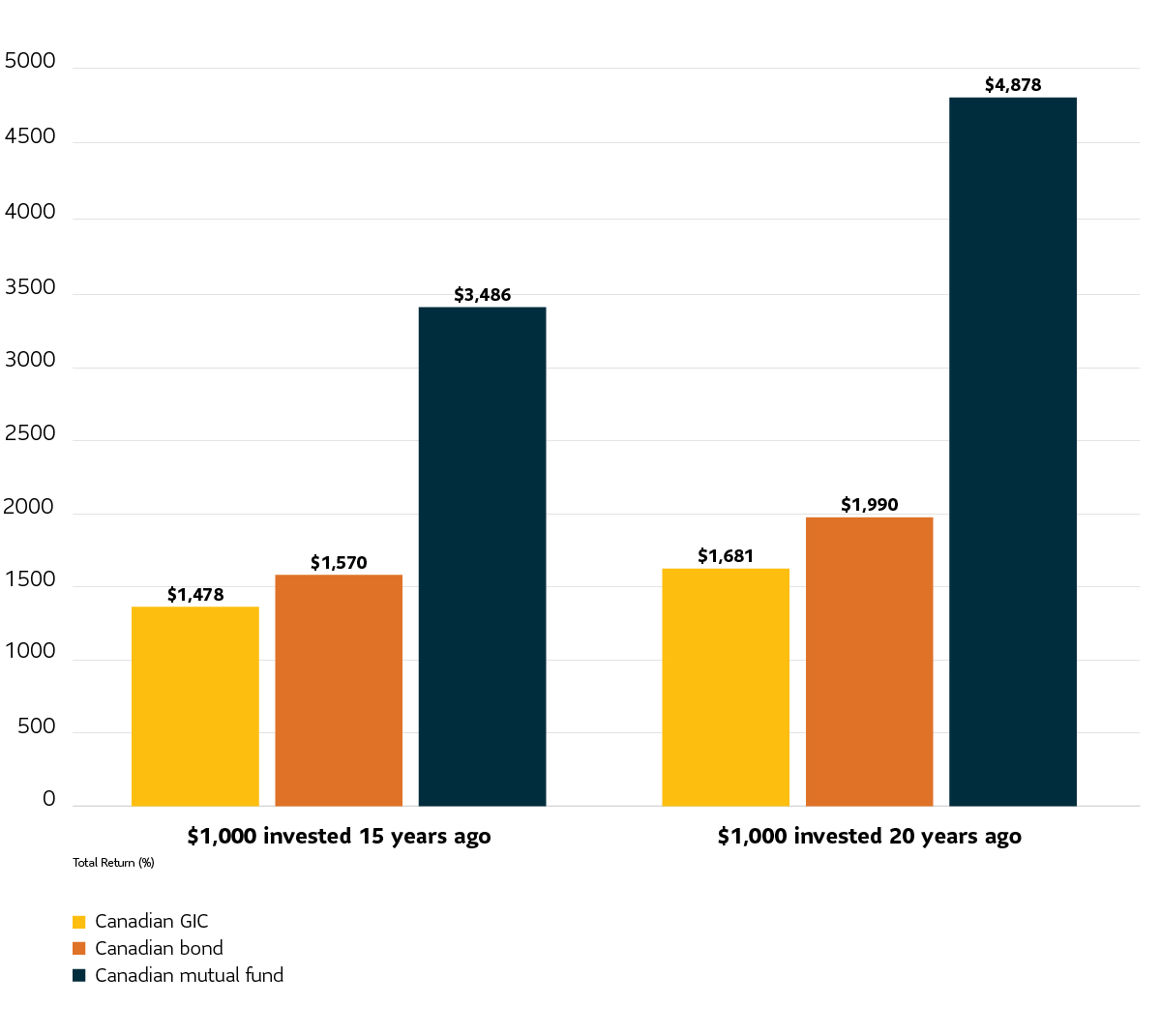

If 15 years ago, you had invested $1,000 in one of these investment vehicles, that amount would now be worth:

- $1,478 in a Canadian 91-day T-bill (2.64% annualized return)

- $1,570 in a Canadian bond (3.15% annualized return)

- $3,486 in a Canadian mutual fund (8.85% annualized return)

- $9,447 in an American mutual fund (16.15% annualized return)

If 20 years ago, you had invested $1,000 in one of these investment vehicles, that amount would now be worth:

- $1,681 in a Canadian 91-day T-bill (2.64% annualized return)

- $1,990 in a Canadian bond (3.5% annualized return)

- $4,878 in a Canadian mutual fund (8.18% annualized return)

- $8,026 in an American mutual fund (10.8% annualized return)

For illustrative purposes only. Returns have been rounded to the nearest whole number for simplicity. Past performance is no guarantee of future results. It is not possible to invest in an index. Actual returns would be different due to fees and expenses associated with investing which are not applicable to an index.

Source: SLGI calculations from Morningstar Direct data, as of May 31, 2025. Returns calculated in Canadian dollars

If you’re concerned and not sure that now is the time, you could consider using a strategy called dollar-cost averaging. This could be a way to move your holdings in a money market fund, for example. into the market in small amounts at a regular pace. You can use our Systematic Transfer Plan (STP) to do your dollar cost averaging. The STP automatically switches a specified dollar amount from a series of securities of one fund to the same series of securities of another fund on a weekly, bi-weekly, semi-monthly, monthly, bi-monthly, quarterly, semi-annual or annual basis.

Read more on the pros and cons of dollar cost averaging.

Information contained in this article is provided for information purposes only. It is not intended to provide or be a substitute for professional, financial, tax, insurance, investment, legal or accounting advice and should not be relied upon in that regard. It also does not constitute a specific offer to buy and/or sell securities. You should always consult your financial advisor or tax specialist before undertaking any of the strategies discussed in this article to ensure that all elements and your personal circumstances are taken into consideration in developing your individual financial plan. Information contained in this article has been compiled from sources believed to be reliable, but no representation or warranty, express or implied, is made with respect to its timeliness or accuracy and SLGI Asset Management Inc. disclaims any responsibility for any loss that may arise as a result of the use of the strategies discussed.