Sun Life ETF+ Portfolios quarterly update

Equity markets had one of their best quarters since Q2 2020, with AI remaining a key performance driver.

Anthony Wu, CFA, Portfolio Manager, Multi-Asset Solutions, SLGI Asset Management Inc.

What happened in the quarter?

The U.S.–Iran conflict remained the defining macroeconomic event of the second quarter (Q2), following a period of elevated geopolitical volatility in Q1. The ongoing conflict drove a surge in energy prices and higher headline inflation. Conditions shifted later in the quarter as ceasefire discussions advanced, leading to a sharp decline in oil prices into quarter end.

Fixed income markets remained under pressure as inflation increased. Global central banks communicated a shift toward tighter monetary policy, with the European Central Bank raising its policy rate during Q2. In the U.S., Kevin Warsh became Chair of the U.S. Federal Reserve on May 22 and has since struck a notably less accommodating tone than markets had expected.

Despite higher inflation risk and the potential for tighter central bank policy, equity markets had one of their best quarters since Q2 2020. Gains were led by technology, with AI remaining a primary catalyst. Demand for AI infrastructure and semiconductors remained robust, driving strong earnings that exceeded expectations across key AI-linked companies and reinforcing confidence in the theme’s durability. SpaceX’s initial public offering (IPO) on June 12 – the largest on record – highlighted strong investor demand for AI and next-generation technology, with shares rising 19.2%1 on the first day of trading. Energy was the weakest sector, reversing earlier gains as oil prices declined with fading geopolitical risk.

International equities underperformed the U.S., with a stronger U.S. dollar weighing on returns. Canadian equities delivered positive returns but lagged the U.S.

1Source: Bloomberg. SpaceX closed its Nasdaq debut on June 12, 2026, at U$160.95 per share from an IPO price of U$135.

| Top contributors/detractors | |

|---|---|

+ Overweight exposure to health care added value. |

- Underweight exposure to information technology and exposure to gold detracted value.1 |

1Indirect exposure to gold is achieved by investing in underlying ETFs that seek to replicate the performance of the price of gold bullion.

What changes did we make?

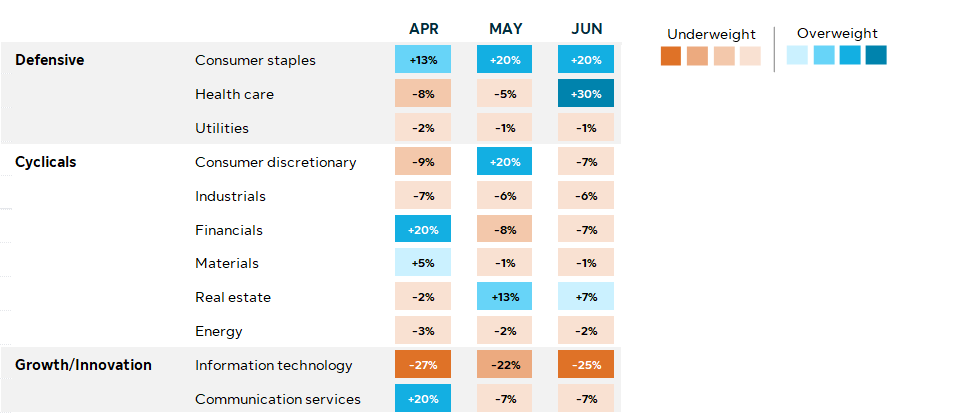

The U.S. sector rotation sleeve was adjusted throughout Q2, as market conditions changed. Following the March U.S. equity market sell-off, we increased exposure to sectors that tend to benefit from improving economic growth and investor confidence, including financials, materials, consumer discretionary and communication services. Returns became highly concentrated in a small group of large technology companies, particularly those benefiting from strong AI-related demand.

By June, we had shifted back toward a more defensive stance – increasing exposure to consumer staples, health care and real estate – as inflation remained elevated and financial conditions tightened. This defensive positioning delivered strong results during the month.

Q2 sector heatmap – Our U.S. sector rotation strategy positioning at a glance

What’s next?

Entering Q3, we’re focused on three themes: central bank policy, the durability of the U.S.–Iran ceasefire, and the strength of the AI-driven equity rally.

June and July inflation data releases across major economies should serve as key indicators of how central banks are likely to respond in the months ahead. While markets are pricing a path for rate hikes, we view this as overstated given the sharp correction in oil prices. If inflation data confirms easing energy price pressures, central banks may have less need to further raise rates, even as services inflation remains elevated.

The rotation away from energy and materials in Q2 reflects falling oil prices as U.S.–Iran ceasefire progress reduced supply risks. The durability of this shift will depend on whether Strait of Hormuz flows normalize and the ceasefire holds. Any re-escalation could reverse recent declines in oil prices and challenge the inflation outlook.

In equities, earnings season should once again be the main test of whether the AI-driven rally remains supported by fundamentals. Late July and August earnings results from major technology companies will be closely watched for continued strength and sustained capital spending on AI infrastructure. Focus is also increasing on AI-driven efficiency gains and their impact on employment, adding a new layer of uncertainty to the broader outlook. All of this could point to greater dispersion in the second half of the year.

View fund performance (Series F)

| Sun Life ETF+ Portfolios advisor materials (log-in required): | Sun Life ETF+ Portfolios Investor material: |

|---|---|

Commissions, trailing commissions, management fees and expenses all may be associated with mutual fund investments. Please read the prospectus before investing. The indicated rates of return are the historical annual compounded total returns including changes in unit value and reinvestment of all dividends or distributions and do not take into account sales, redemption, distribution or optional charges or income taxes payable by any security holder that would have reduced returns. Mutual funds are not guaranteed, their values change frequently and past performance may not be repeated.

Views expressed regarding a particular company, security, industry or market sector should not be considered an indication of trading intent of any mutual funds managed by SLGI Asset Management Inc. These views are subject to change and are not to be considered as investment advice nor should they be considered a recommendation to buy or sell. This commentary is provided for information purposes only and is not intended to provide specific individual financial, investment, tax or legal advice. Information contained in this commentary has been compiled from sources believed to be reliable, but no representation or warranty, express or implied, is made with respect to its timeliness or accuracy.

Information contained in this commentary has been compiled from sources believed to be reliable, but no representation or warranty, express or implied, is made with respect to its timeliness or accuracy. Mutual funds transact daily, and the metrics presented may change at any time, without notice. This commentary may contain forward-looking statements about the economy, and markets; their future performance, strategies or prospects. The words “may,” “could,” “should,” “would,” “suspect,” “outlook,” “believe,” “plan,” “anticipate,” “estimate,” “expect,” “intend,” “forecast,” “objective” and similar expressions are intended to identify forward-looking statements. Forward-looking statements are not guarantees of future performance and are speculative in nature and cannot be relied upon. Forward-looking statements involve inherent risks and uncertainties about general economic factors, so it is possible that predictions, forecasts, projections and other forward-looking statements will not be achieved. You are cautioned to not place undue reliance on these statements as a number of important factors could cause actual events or results to differ materially from those expressed or implied in any forward-looking statement. Before making any investment decisions, you are encouraged consider these and other factors carefully.