Q2 2024 | Market Update

A gradual cooling of jobs and a slowdown in consumer prices improved the chances that major economies will avoid a recession. Looser monetary policy from major central banks is adding to hopes that equities will continue to climb.

Highlights

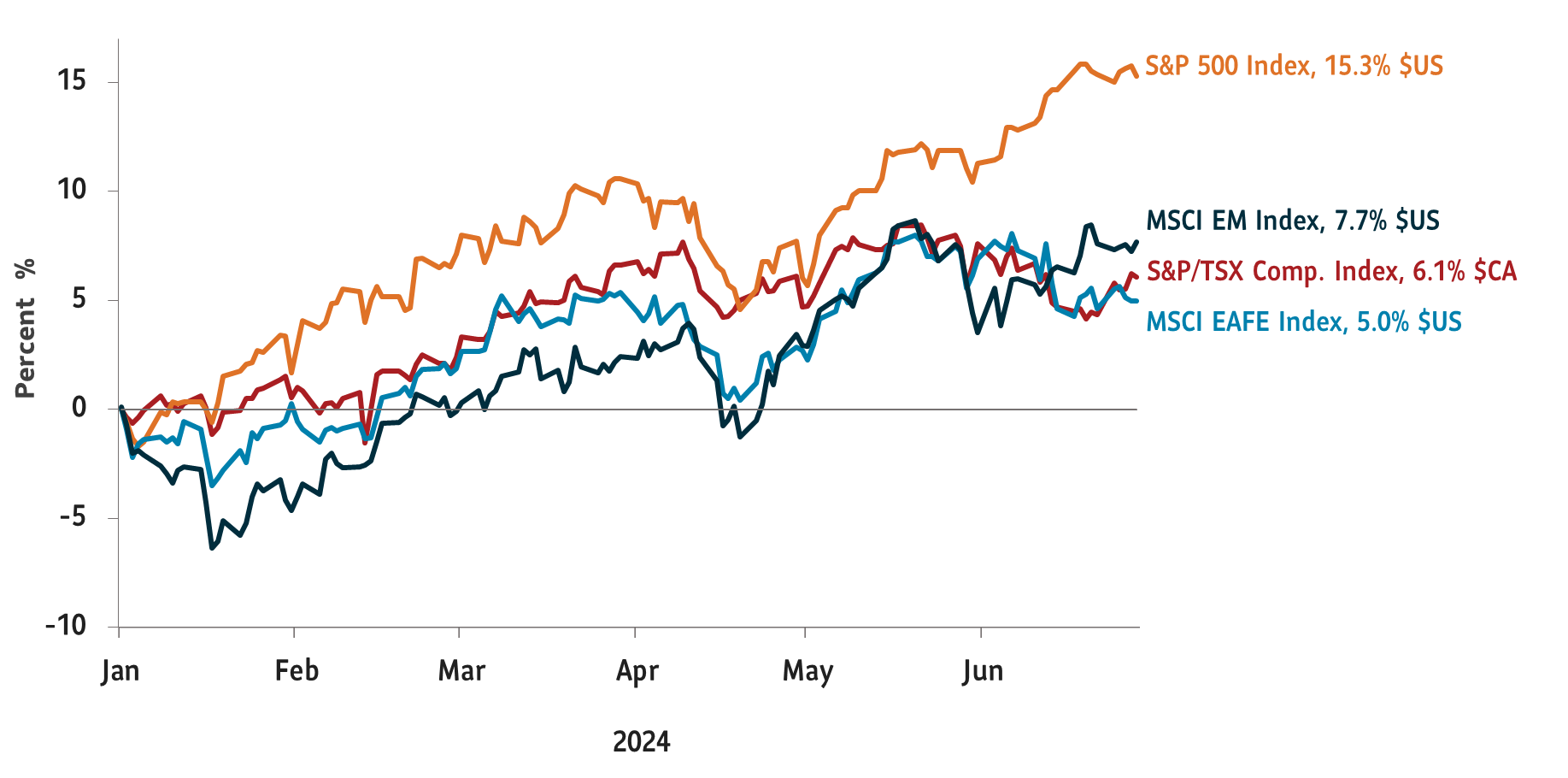

- The S&P 500 and Nasdaq Composite rose 15.3% and 17.3% for the first six months of 2024

- The S&P TSX Composite increased 6% for the first six months of this year

- The U.S. unemployment rate inched up to 4.1% in June 2024 compared to 3.6% a year ago, adding to signs that the labour market is easing

- U.S. consumer prices started trending down again in Q2 2024 after surprising to the upside in Q1 2024

- Canada’s unemployment rate rose to 6.4% in June 2024 and has been on a gradual upward trend since April of last year

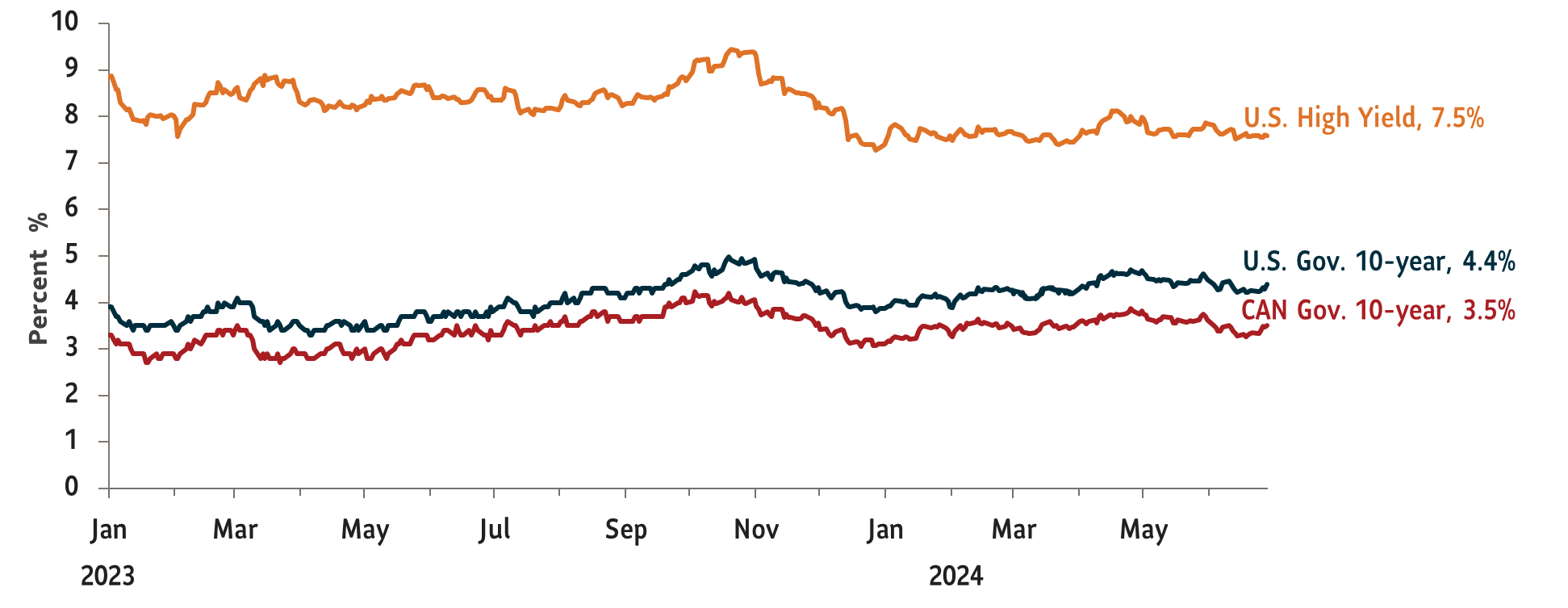

- The European Central Bank and the Bank of Canada initiated interest rate cuts in Q2 2024 as concerns over economic growth grew

Markets soar in first half of 2024 fueled by higher hopes of a “soft-landing”

U.S. equity markets had a banner first half of 2024. The benchmark S&P 500 Index rose 4.4% in Q2 2024 for total gains of 15.3% for the first six months of the year. The tech-heavy Nasdaq Composite Index did even better, up 17.3% for the six-month period ending June 30, 2024. While investors’ enthusiasm about artificial intelligence has driven equities higher over the past 18 months, macroeconomic trends of gradual cooling in the U.S. job market alongside a slowdown in inflation have recently boosted markets even further. While the U.S. has continued to add jobs, the pace of jobs growth has slowed, and the unemployment rate has inched up to 4.1%. On the other hand, thanks to tight monetary policy from the U.S. Federal Reserve (the Fed), prices are showing a disinflationary trend. Markets now expect the Fed to cut interest rates twice before the end of 2024.

Equity markets rallied in Q2 2024

Total return, indexed to 0 as of January 1, 2024

Source: Bloomberg. Data as of June 30, 2024.

We think conditions are right for the Fed to initiate a rate cut within the next six months. Our research shows that the U.S. consumer price index (CPI) could start to capture the slowdown in shelter inflation over the next few months. We expect this to confirm the further disinflationary trend required for the Fed to cut borrowing costs. We also expect the U.S. consumer to come under more strain as pandemic-era savings dwindle, job growth shrinks and wage gains slow. This along with a lukewarm manufacturing sector in the U.S. could force the Fed to prioritize growth and jobs in the coming months.

Bond yields relented a bit in Q2 2024

U.S. and Canada 10-year bond yields

Source: Bloomberg. Data as of June 30, 2024.

We are concerned about economic growth prospects outside the U.S. Government spending has been an extra boost for U.S. growth, but an absence of such fiscal generosity in other economies is already showing. Many developed economies are wrestling with a more acute manufacturing slowdown than the U.S. Other sources of growth such as consumption and exports are also under pressure outside of the U.S. In response, major central banks such as the European Central Bank and the Bank of Canada have already initiated interest rate cuts to loosen monetary conditions.

Given these conditions and geopolitical risks, we are largely neutral to equities across regions. In the U.S., we are concerned about the concentration of gains in the technology sector, where a handful of stocks have largely driven market returns. We also worry about the rich valuations of U.S. equities relative to their profit outlook. On the other hand, we think the equity rally may broaden out to sectors that have mostly been stagnant for many quarters. We think a Fed rate cut may give a much-needed boost to these sectors. We also reduced our bets on emerging market equities as our data shows rising growth concerns. Within fixed income, we think core credit dominated by government issuers offer more value over risky credit such as high-yield that are trading at tighter spreads. We are modestly overweight cash as we look for opportunities to deploy in both equity and fixed income markets.

Views expressed regarding a particular company, security, industry or market sector should not be considered an indication of trading intent of any mutual funds managed by SLGI Asset Management Inc. These views are subject to change and are not to be considered as investment advice nor should they be considered a recommendation to buy or sell. This commentary is provided for information purposes only and is not intended to provide specific individual financial, investment, tax or legal advice. Information contained in this commentary has been compiled from sources believed to be reliable, but no representation or warranty, express or implied, is made with respect to its timeliness or accuracy.

This commentary may contain forward-looking statements about the economy and markets, their future performance, strategies or prospects or events and are subject to uncertainties that could cause actual results to differ materially from those expressed or implied in such statements. Forward-looking statements are not guarantees of future performance and are speculative in nature and cannot be relied upon.