Q3 2024 | Market Update

We think the chances of a U.S. soft landing - a scenario of bringing down inflation to around 2% without widespread job losses - has improved. Our tactical position favours a slight overweight to equities and commodities as the U.S. economy slowly sheds the weight of high levels of real interest rates.

Highlights

- After subdued data reports in early Q3 2024, the U.S. labour market ended the quarter with healthy jobs numbers and a low unemployment rate of 4.1%.

- The U.S. Consumer Price Index continued to rise at a slower pace - 2.4% in September.

- While survey data like consumer and business confidence remains lukewarm, hard data such as real income and consumption growth in the U.S. remains healthy.

- The U.S. Federal Reserve has pivoted to interest rate cuts even as the economy continues to be resilient. We think this has increased the chances of a soft landing for the U.S. economy.

Robust markets continue as the U.S. Fed pivots to interest rate cuts amid a resilient economy

U.S. equity markets continued to march higher in Q3 2024. Despite bouts of volatility in the wake of slowing jobs growth in July and August, stocks were buoyed by the U.S. Federal Reserve’s (the Fed) decision to cut interest rates by 50 basis points (bps) to a range of 4.75% and 5.00% in September 2024. The rate cut, the first in over four years, came as the Fed shifted its focus from fighting inflation to preserving jobs. Stocks were boosted by stellar jobs growth in September, which reassured markets that U.S. labour remained healthy even as inflation continued to rise at a slower pace.

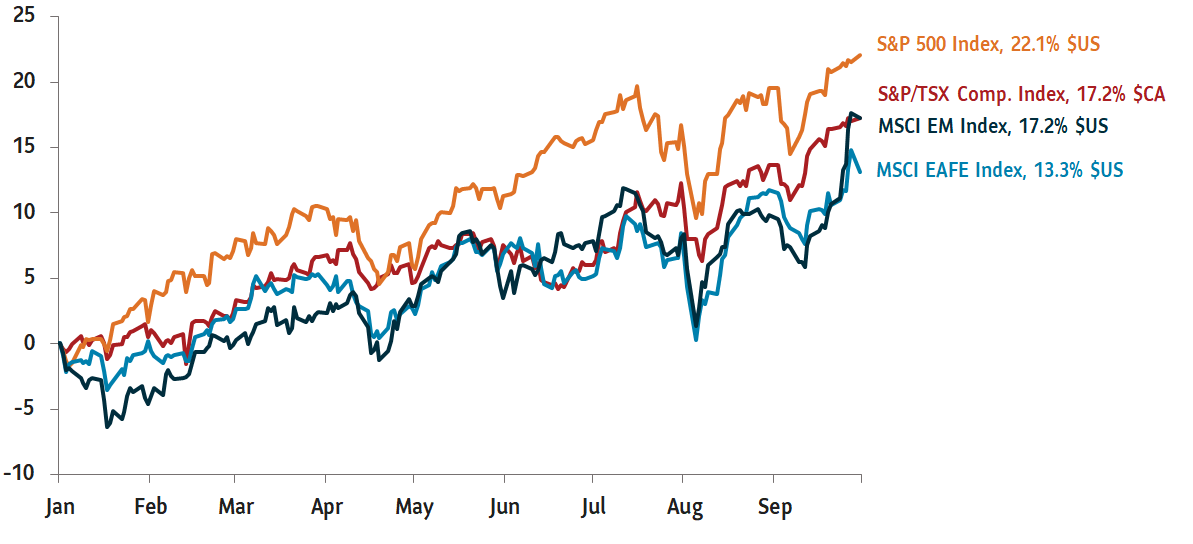

The benchmark S&P 500 Index, which continued to hit record highs in the first half of 2024, rose another 5% during Q3 2024 - up nearly 22.1% for the first nine months this year. The Nasdaq Composite Index climbed over 23% for the first nine months of 2024, powered by the technology sector.

Chart 1: Equity markets rallied in Q3 2024

Total return, indexed to 0 as of January 1, 2024

Source: Bloomberg. Data as of September 30, 2024.

We think the chances of a soft landing for the U.S. has improved. With the Fed’s decision to cut the policy rate, real interest rates are likely to be less restrictive going forward. While both businesses and consumers in the U.S. are cautious about their outlook for the U.S. economy, hard data such as the growth in real personal income and consumption tell a story of a resilient economy. Even cyclical parts of the economy, which usually weaken prior to a recession, seem in decent shape. Indicators such as auto dealership payrolls and temporary labour force numbers do not show signs of a recession. This gives us confidence that the U.S. can avoid a hard landing. But we think the rest of the world’s economy is weaker than the U.S. Growth in the Euro zone has been feeble in recent quarters as the region’s largest economies, Germany and France, grow at a slower pace. However, equity valuations in the region is reasonable and we think equities could get a modest lift as the European Central Bank cuts interest rates. Structural factors continue to pose a challenge to China’s growth despite recent efforts to stimulate its economy.

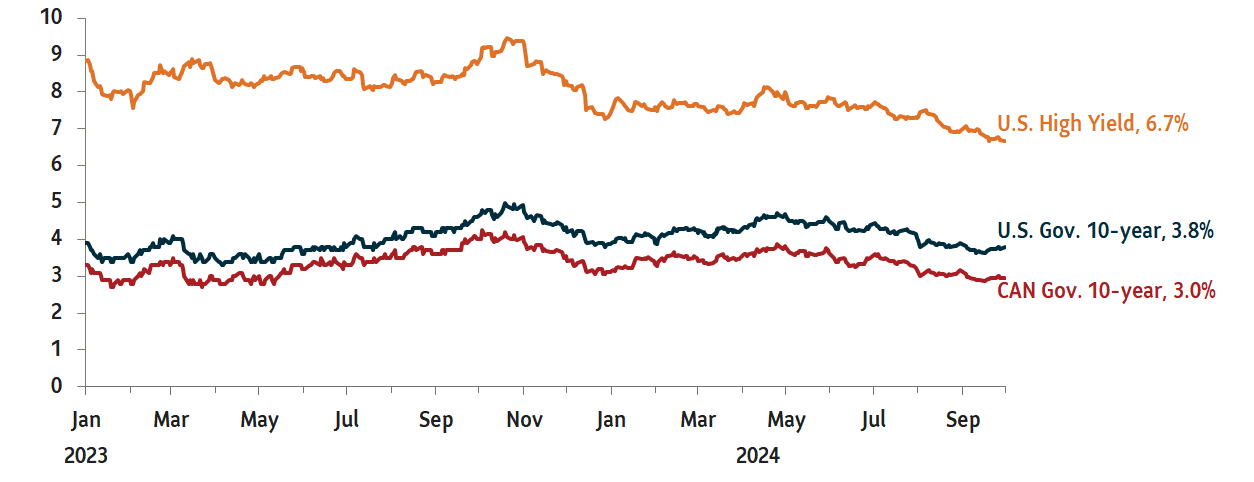

Chart 2: Bond yields in Q3 2024

U.S. and Canada 10-year bond yield

Source: Bloomberg. Data as of September 30, 2024.

While the U.S. economy has been strong, we are concerned about record deficits in the country. U.S. budget deficits now equal about 7% of GDP in 2024, a record figure for an expansionary phase of the economy. While such deficits may be sustainable in the short term, we fear bond markets could quickly turn volatile in the medium-term should certain tail risks materialize.

As for our tactical positioning, we hold a modest overweight position to U.S. equities as we think the U.S economy may avoid a recession. While equity valuations are still high in the U.S., we think valuations are not unreasonable outside the technology sector. We are also modestly overweight international equities as the rate-cutting cycle could provide a tailwind to these assets. We also hold an overweight position in commodities. We think an exposure to precious metals such as gold could be a good hedge to equities should a recession materialize or should inflation rise again. We are also neutral towards bonds.

Views expressed regarding a particular company, security, industry or market sector should not be considered an indication of trading intent of any mutual funds managed by SLGI Asset Management Inc. These views are subject to change and are not to be considered as investment advice nor should they be considered a recommendation to buy or sell. This commentary is provided for information purposes only and is not intended to provide specific individual financial, investment, tax or legal advice. Information contained in this commentary has been compiled from sources believed to be reliable, but no representation or warranty, express or implied, is made with respect to its timeliness or accuracy.

This commentary may contain forward-looking statements about the economy and markets, their future performance, strategies or prospects or events and are subject to uncertainties that could cause actual results to differ materially from those expressed or implied in such statements. Forward-looking statements are not guarantees of future performance and are speculative in nature and cannot be relied upon.