Q4 2024 | Market Update

The S&P 500 climbed over 60% for the two-year period between 2023 and 2024, the best in a quarter century. But it turned volatile in early 2025. While markets have concerns over the future of interest rate cuts from the Fed, we are tactically bullish on equities as earnings growth broadens amid a resilient U.S. economy.

Highlights

- The U.S. labour market finished 2024 on a high note with a 4.1% unemployment rate in December. While U.S. job gains slowed to 2.2 million in 2024 from about 3 million the previous year, this still beats 2 million from 2019.

- We think a “no landing” scenario of resilient growth and a bit of sticky inflation as a likely outcome for the U.S. economy.

- Buoyed by a resilient U.S. economy, the benchmark S&P 500 Index had its best two-year performance since 1998. We expect this strength to continue despite bouts of volatility.

- Canada’s economy, which slowed considerably in 2024, showed signs of stability in late 2024.

- But uncertainties surrounding the Trump administration’s tariff policy and a weak Canadian dollar could influence the Bank of Canada’s interest rate policy in 2025.

2025 begins with worries about future rate cuts, after 2024’s equity bull market

U.S. equities advanced at a rapid pace in 2024 and finished the calendar year with robust gains. Slowing but resilient labour markets, interest rate cuts from the U.S. Federal Reserve (the Fed), and ongoing enthusiasm for artificial intelligence and information technology stocks fueled U.S. stocks. Expectations of pro-growth policies such as tax cuts and deregulation from the incoming Trump administration further supercharged markets.

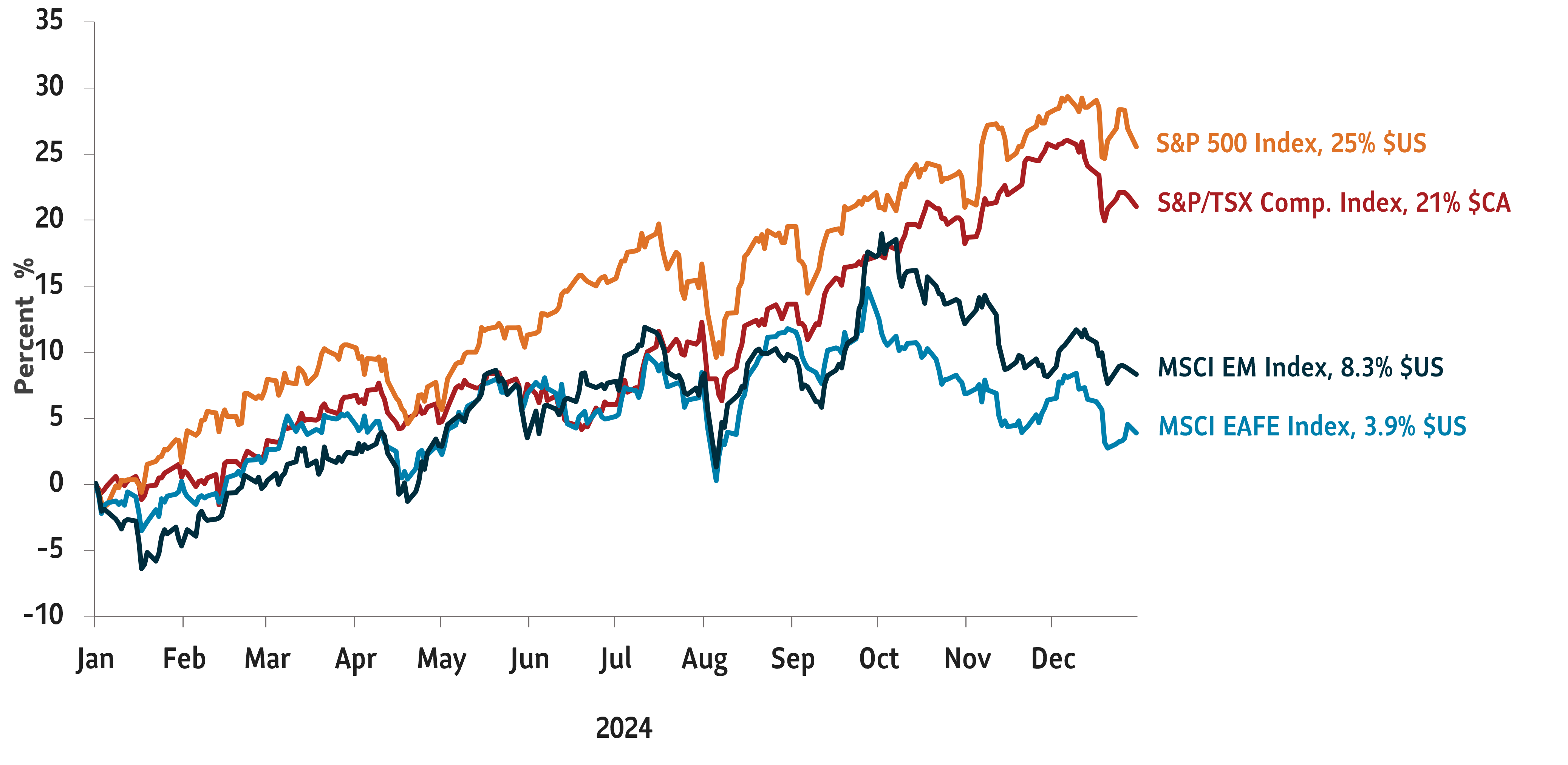

As a result, despite a volatile December, the benchmark S&P 500 Index rose 25% in 2024 after increasing 26% the previous year. This was the S&P 500’s best two-year performance since 1997 and 1998. Other assets joined the party: gold had its best year since 2010, and international equities represented by the MSCI All Country World Index jumped 16%. At home, Canada’s S&P TSX index rose 21% in 2024 on a total return basis.

Equity markets rallied in Q4 2024

Total return, indexed to 0 as of January 1, 2024

Source: Bloomberg. Data as of Dec 31, 2024.

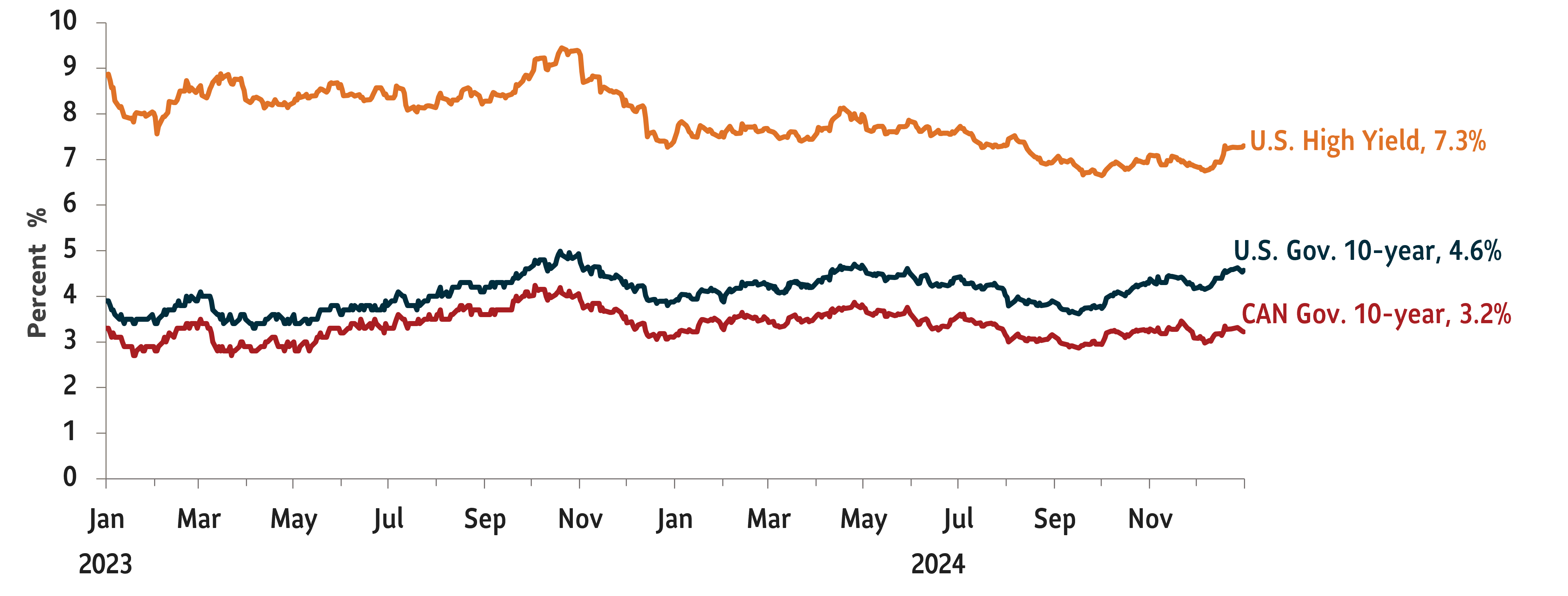

However, the rally bypassed one key asset class: bonds. While bonds measured by the Morningstar US Core Bond Index gained a mere 1.36% (US$ terms) in 2024, a rapid rise in 10-year U.S. Treasury yields wiped out a significant part of their gains during Q4 2024. The same pro-growth policy expectations from the Trump administration that buoyed stocks have hurt bonds. Markets expect Trump’s economic policies to further add to the country’s fiscal deficit and hinder the Fed’s fight against inflation. As a result, 10-year Treasury yields, which hovered around 3.6% in September, rapidly rose to 4.6% by the end of 2024. They further jumped to a 14-month high of 4.8% in January 2025. Markets now expect the Fed to pare back interest rate cuts in 2025.

Bond yields climbed briskly in Q4 2024

U.S. and Canada 10-year bond yields

Source: Bloomberg. Data as of December 31, 2024.

We think markets are correct in reducing their expectations of upcoming interest rate cuts from the Fed. December’s labour market report confirmed our predictions that the U.S. economy is in good shape. A gain of about 256,000 jobs in December, a low unemployment rate of 4.1%, and inflation stuck between 2% and 3% alongside lower immigration could warrant fewer rate cuts. We now think a “no landing” scenario - resilient growth and inflation slightly above target - as the most likely outcome for the U.S. over the next few quarters. We expect the Bank of Canada to cut rates twice in the first half of 2025 as it tries to balance slowdown worries against a falling domestic currency.

As for our tactical positioning, we are overweight U.S. equities. Some of our sentiment models have indicated that markets are overly pessimistic despite positive economic data. Within equities, we are positive on the U.S. semiconductor sector, where earnings growth has risen to meet expectations and momentum continues. While valuations have trended higher for large cap technology stocks, we expect the earnings growth and rally to broaden to other sectors. While we are largely neutral on bonds, we think they’re getting more attractive despite a chance that yields may rise a bit from current levels.

Views expressed regarding a particular company, security, industry or market sector should not be considered an indication of trading intent of any mutual funds managed by SLGI Asset Management Inc. These views are subject to change and are not to be considered as investment advice nor should they be considered a recommendation to buy or sell. This commentary is provided for information purposes only and is not intended to provide specific individual financial, investment, tax or legal advice. Information contained in this commentary has been compiled from sources believed to be reliable, but no representation or warranty, express or implied, is made with respect to its timeliness or accuracy.

This commentary may contain forward-looking statements about the economy and markets, their future performance, strategies or prospects or events and are subject to uncertainties that could cause actual results to differ materially from those expressed or implied in such statements. Forward-looking statements are not guarantees of future performance and are speculative in nature and cannot be relied upon.