Fund facts guide

A guide to understanding your mutual fund investment

The facts explained

The fund facts document is a clear, plain language document that contains key information about the mutual fund you’re thinking about purchasing. In no more than two double-sided pages, it explains the basics of what the fund invests in, the risks involved, how the fund has performed, and the costs of ownership. Review the fund facts document with your advisor and don’t be afraid to ask questions. It’s important that you’re comfortable with your investment decision.

Mutual funds are often available in different series. All series of a fund will have the same investment objective, but may have different availability based on the type of investor and his or her individual goals. For example, SLGI Asset Management Inc. offers Series A to all investors, but offers Series I only to institutional investors.

This is the date the fund facts document was filed with securities regulators. Fund facts documents are required to be updated every year and any time there’s a material change to the fund.

It’s important to understand how a particular fund fits into your overall financial plan and with your other investments. Your advisor will work with you to determine if this investment is suitable for you.

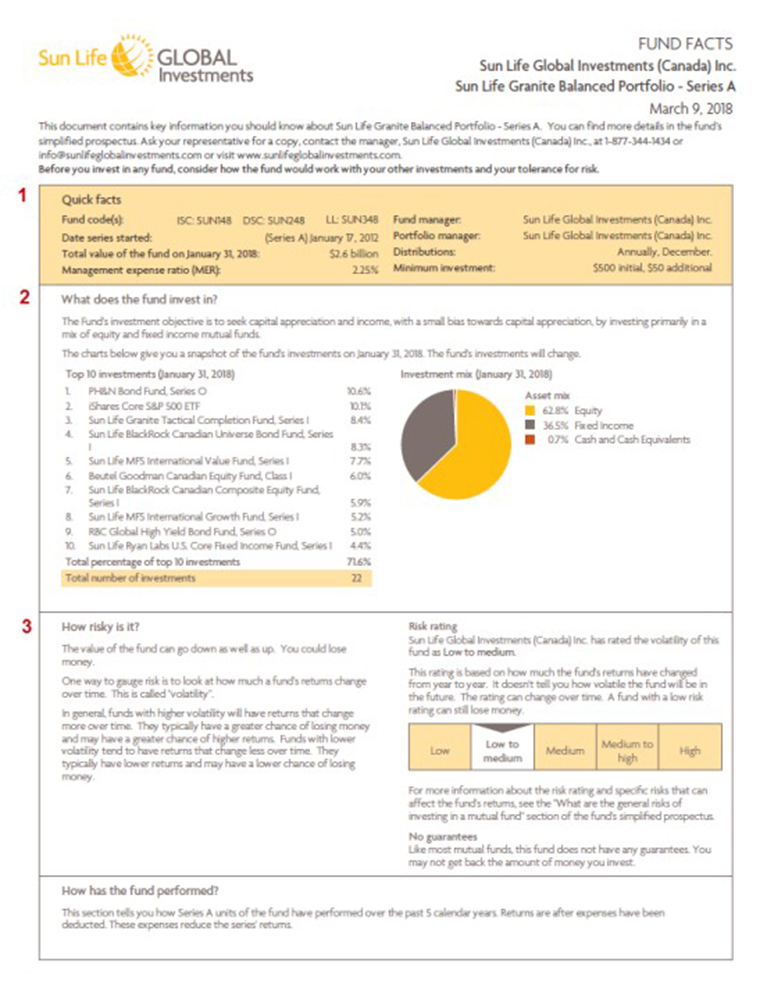

(1) Quick Facts

Date series started: The date this particular series of the fund first became available for purchase, also known as the “inception date.”

Total value of the fund: This is the total amount of money invested in the fund from all investors in all series of the fund as of the date specified.

Management expense ratio (MER): This percentage represents the ongoing cost of owning the fund. It’s made up of the fund’s management fee and operational expenses. MERs will vary from fund to fund and from series to series.

Fund manager: Responsible for the day-to-day business and operations of the fund.

Portfolio manager: Manages the investment portfolio of the fund.

Distributions: This tells you if, when, and how frequently this series of the fund expects to pay a distribution.

Minimum investment: The amount required for a first-time investment, as well as any subsequent purchases of the same fund.

(2) What does the fund invest in?

This section describes what the fund invests in and also provides some information about the actual investments within the fund, also called “holdings”. Depending on the type of fund, you may be able to see how much of the fund is invested in stocks versus bonds, the geographic breakdown, and/or the industry sector breakdown. You will also see the ten investments that make up the fund’s largest holdings.

(3) How risky is it?

In this section, it’s made clear that the value of the fund can go down as well as up, and that you could lose money. There is also a risk rating of the fund, using a risk scale that ranges from “Low” to “High”. Additional risks are defined more thoroughly in the prospectus.

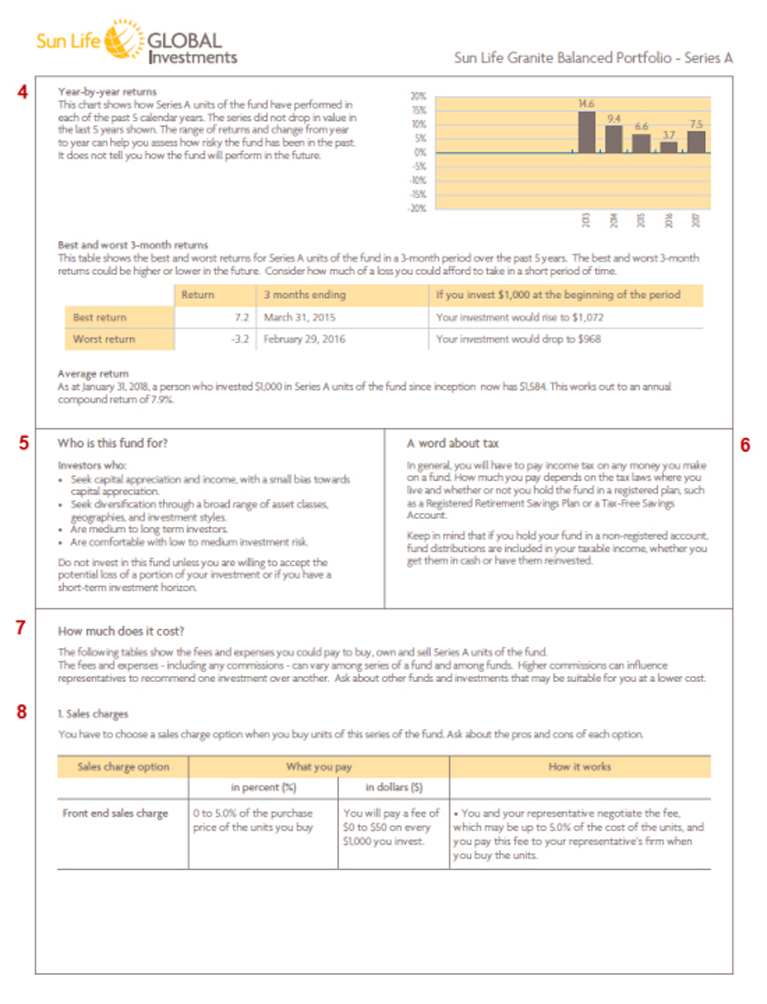

How has the fund performed?

This section gives you three different views on how the fund has performed, assuming all distributions are reinvested. It does not tell you how well the fund will perform in the future.

(4) Year-by-year returns:

See how the fund has performed in percentage terms on a calendar-year basis over the past ten years, provided the fund has been in existence for that length of time.

Best and worst 3-month returns: Measured over the length of time the fund has existed, this metric is an indicator of short-term volatility. It’s intended to encourage you to consider how much of a loss you could afford to take in a short period of time.

Average return: See how much the fund has gained or lost since it was first created, in dollar terms. Also learn how much it’s gained or lost on an annual basis, in percentage terms.

(5) Who is this fund for?

These are the characteristics of an investor for whom the fund may or may not be suitable. Work with your advisor to determine whether the fund is suitable for you.

(6) A word about tax

General information about the tax impact of investing in the fund. Begin the conversation about tax with your advisor, and consider speaking to a tax expert if you have further questions.

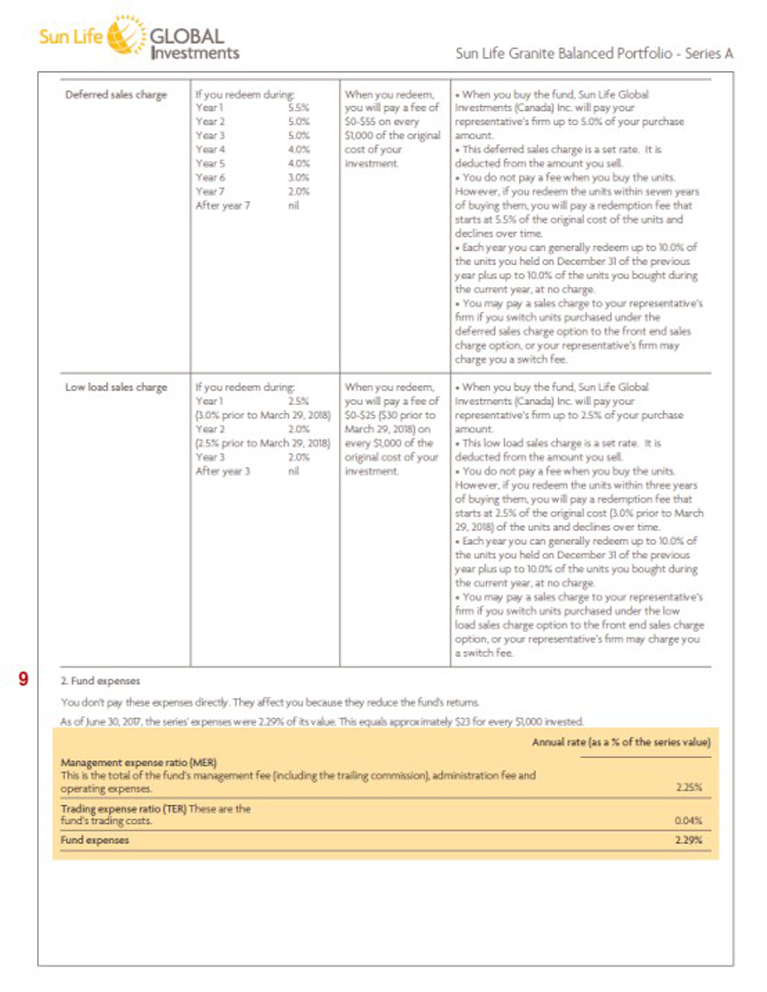

(7) How much does it cost?

Understanding the cost of purchasing, owning, and selling mutual funds is important. Different investment types, including different series of the same mutual fund, and different fee structures within each series, might be more or less appropriate based on your goals and personal circumstances.

(8) Sales charges

Different mutual funds come with different sales charge options. Depending on which option you choose, you may or may not pay a sales charge. Work with your advisor to determine a sales charge option that suits your goals, time horizon, and risk tolerance.

(9) Fund expenses

Fund expenses are so called because they’re paid by the fund, not by you. They affect you because they reduce the fund’s returns.

The management expense ratio (MER) first identified in the Quick Facts section is further explained here.

The trading expense ratio (TER) captures the cost of buying and selling securities within the fund. The more frequently a fund buys and sells securities, typically with the goal of outperforming a certain benchmark index, the higher the TER.

Together, the MER and TER make up the fund expenses.

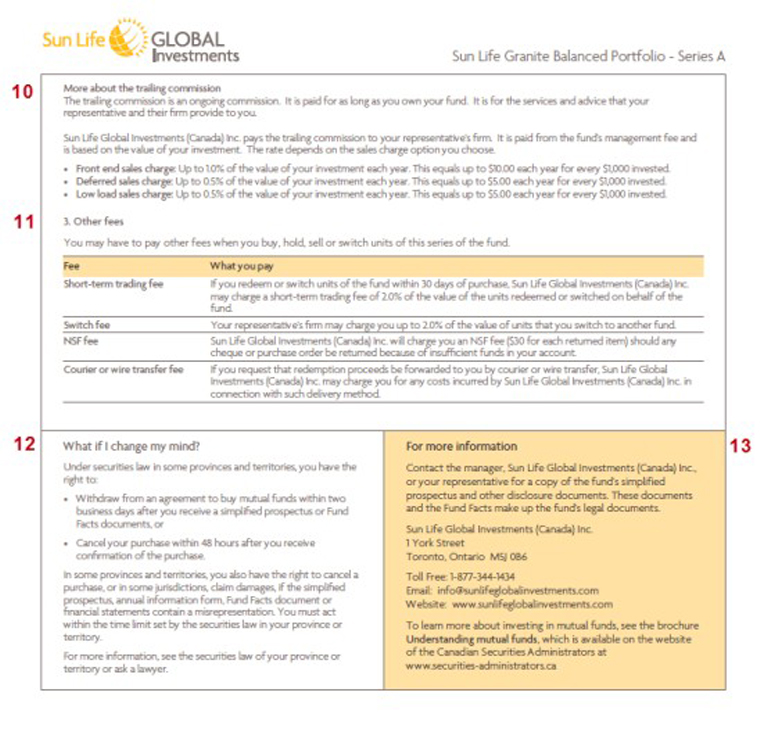

(10) More about the trailing commission

This section explains the trailing commission in more detail. The trailing commission is often paid by the investment fund manager to the mutual fund dealer, which is the firm that services your account. The dealer pays a portion of the trailing commission to its representative – your advisor. The amount of the trailing commission depends on the sales charge option you choose.

Ask your advisor to explain the services he or she provides in exchange for this commission.

(11) Other fees

There may be fees other than sales charges associated with your account activities, some of which are intended to discourage short-term trading.

(12) What if I change my mind?

Before you make a purchase, understand what your options are if you change your mind within a certain time frame.

(13) For more information

Your advisor is likely your primary resource for questions you may have about your investments. After all, your advisor is the one most familiar with your financial situation. You have other resources as well, some of which are identified in this section.

For more about the fund facts document, or if you have general questions about investing in mutual funds, speak with your advisor.

Commissions, trailing commissions, sales charges, management fees and expenses all may be associated with mutual fund investments. Please read the prospectus for details before investing. Mutual funds are generally not guaranteed, their values may change frequently and past performance may not be repeated.