Why Canadian banks are largely immune to a bank run

Strong regulation, supervision and a conservative risk culture characterize Canada’s concentrated banking industry. This has reinforced the message that Canadian banks are safe following recent bank runs in the U.S.

By Christine Tan, CFA, Portfolio Manager, SLGI Asset Management Inc.

Bank runs used to start with worried account holders lining up at bank branches, desperate to get their money. Now in the digital age, bank runs begin with a few taps to a banking app on a smartphone. As concerns about the solvency of Silicon Valley Bank (SVB) in the U.S. circulated in social media, over USD$40 billion in deposits fled the bank within hours. Soon customers in other U.S. regional banks followed, which underscores the fragility and interconnection of the banking system.

While we think the problems related to SVB are unique, we also think Canadian banks are unlikely to suffer a SVB-style bank run. One key reason is Canadian banks are easier to supervise because there are only 85 banks in Canada and six of the country’s largest banks account for over 85% the industry’s assets. In the U.S. there are over 4,700 banks1.

Not just well-regulated but also well-supervised

Banking is an inherently risky business. Loans or investments made by a bank can go bad resulting in credit defaults. These concerns could lead depositors to fear the safety of the bank and withdraw their deposits resulting in liquidity risk. A bank run is an extreme form of liquidity risk.

In simple terms, banks take in money and make loans or investments to earn a profit.

Example: Bank A collects CAD$1 billion from 10,000 depositors that it promises to repay on demand. This is a “liability” because Bank A has to repay it. It then loans that CAD$1 billion to 10 companies to be repaid with interest over a five-year period. This is an “asset” for the bank because it will earn interest on it until borrowers pay it back.

This simple banking model example illustrates an asset-liability mismatch

The 10,000 depositors can demand their funds all at once overnight, but the bank can’t quickly recall the 5-year loans made to companies. Banks are very aware of this risk. That’s why they seek funding from depositors and investors with longer-term commitments like term-deposits, bonds and equities. This can be expensive but helps to better address their asset-liability mismatch.

Canada’s banking regulator, the Office of the Superintendent of Financial Institutions (OSFI) requires its six largest banks to keep their Common Equity Tier 1(CET 1) capital – long-term capital – above 11%. OSFI also holds a tight leash on its medium-sized banks (MSB) and requires them to maintain a CET 1 capital above 7%. These stringent capital requirements ensure Canadian banks can deal with credit or investment losses in times of economic downturn.

A strong risk culture

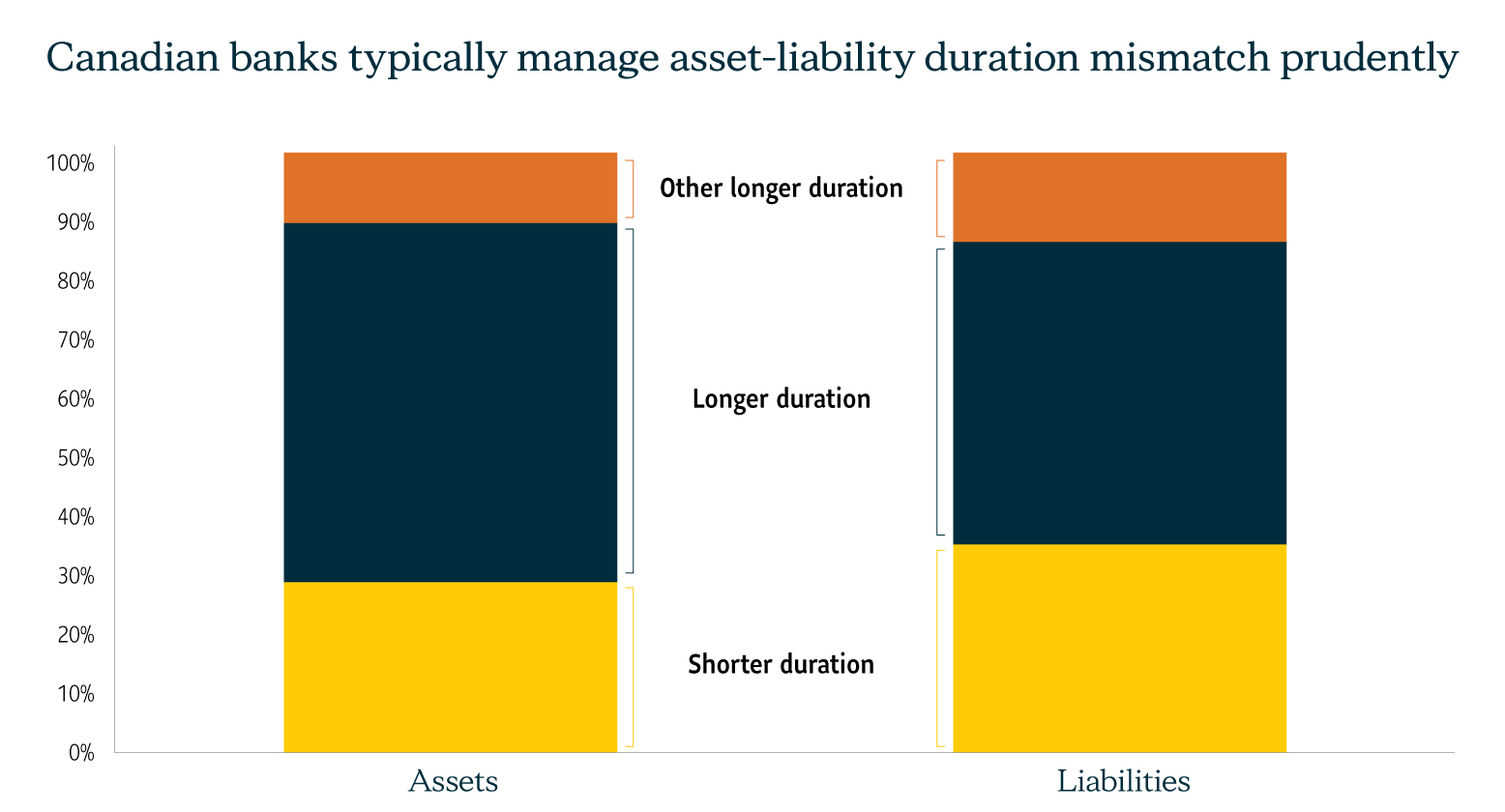

For their part, Canadian banks have historically managed their balance sheet risks prudently. Canadian banks’ lending activities are generally well-diversified across sectors. The banking industry’s longer-term assets (loans and investments) are relatively well-matched by conservatively managed liabilities (funds raised from depositors and bondholders) and shareholder equity.

Source: Consolidated monthly balance sheet for all Canadian banks, January 31, 2023. Office of the Superintendent of Financial Institutions (OSFI)* Please refer to footnotes for details about the various categories of assets and liabilities.

In addition, Canadian banks have managed their securities investments more carefully over the years. This is where banks make money by investing short-term proceeds into longer-term bonds at higher yields. It’s also the portfolio subject to interest rate risk. When interest rates started to rise sharply in 2022, these securities portfolios suffered losses. As long as these portfolios aren’t sold at a loss, banks typically don’t have to realize losses against their profits. Unrealized losses as a percentage of total assets stood at 8.4% for SVB, while Canadian banks averaged at a very manageable 0.3%2.

But a case of liquidity shortfall can force a bank to sell these assets at a loss and immediately hurt its retained earnings, which is part CET-1 capital. In the case of SVB, selling securities at a loss erased a lot of its equity and eventually led to government intervention to prevent full failure. We see such risks unlikely with Canadian banks.

The combination of strong regulation supervision, well-managed risks, and an industry structure favouring big banks largely protect the Canadian banking industry from bank failures.

The immediate fear triggered by SVB has subsided and both the US Federal Reserve and the Federal Deposit Insurance Corp (FDIC) have taken steps to reassure Americans. But the longer-term impact of the recent bank failures could lead to U.S. banks reducing their lending activity to offset deposit outflows or further declines in its investments. We think that this tightening has increased the risk of, and accelerated the potential onset, of a U.S. recession.

1,2 Canadian Banking Sector: Market Volatility Continues, but Funding Is Stable and Unrealized Losses Appear Manageable, Morningstar DBRS, March 20, 2023.

*Shorter duration assets include cash and cash equivalents, Canadian Federal, Provincial, Municipal or School Corp securities, less expected credit losses and other securities less allowance for expected credit losses.

Short-duration liabilities include government & financial institutions demand and notice deposits, individuals demand and notice deposits and other demand and notice deposits.

Longer duration assets include non-mortgage loans and mortgages less allowance for expected credit losses. Longer duration liabilities include fixed term deposits, subordinated debt, and obligations related to borrowed securities and assets sold under repurchase agreements. Shareholder’s equity is classified as longer duration. Interests in associates and joint ventures, deferred tax assets and other assets are classified under other longer duration assets. Other longer duration liabilities include mortgages and loan payables.

Views expressed regarding a particular company, security, industry or market sector should not be considered an indication of trading intent of any mutual funds managed by SLGI Asset Management Inc. These views are subject to change at any time and are not to be considered as investment advice nor should they be considered a recommendation to buy or sell.